Unraveling the Mysteries: Loan Terms and Interest Calculations! ===

Loans play a significant role in our lives, helping us finance our dreams and achieve our goals. However, understanding the intricacies of loan terms and interest calculations can often feel like navigating a labyrinth. Fear not, for in this article, we will embark on a delightful journey into the world of loans and unravel the mysteries of how loan terms affect interest calculations. Through a comparative analysis, we will shed light on various aspects that can influence the total interest payable. So let’s dive in and discover the secrets that lie within the realm of loans!

A Dive into the World of Loans: Comparative Analysis Sheds Light!

When it comes to loans, the terms and conditions can vary significantly. From the interest rate to the repayment period, each element can have a profound impact on the total amount of interest paid over the loan’s duration. Let’s explore how different loan terms can affect interest calculations by diving into a comparative analysis.

Firstly, the interest rate plays a crucial role in determining the total interest paid. A higher interest rate will result in a larger interest burden, increasing the overall cost of the loan. Conversely, a lower interest rate can save borrowers a substantial amount of money. It is essential to compare interest rates offered by different lenders before choosing a loan to ensure the most favorable terms are obtained.

Secondly, the repayment period is another vital factor that affects interest calculations. Generally, a longer repayment period will result in higher interest costs, as the interest accrues for a more extended period. On the other hand, opting for a shorter repayment period could mean higher monthly payments but reduced overall interest paid. It is crucial to strike a balance between manageable monthly payments and minimizing the interest burden.

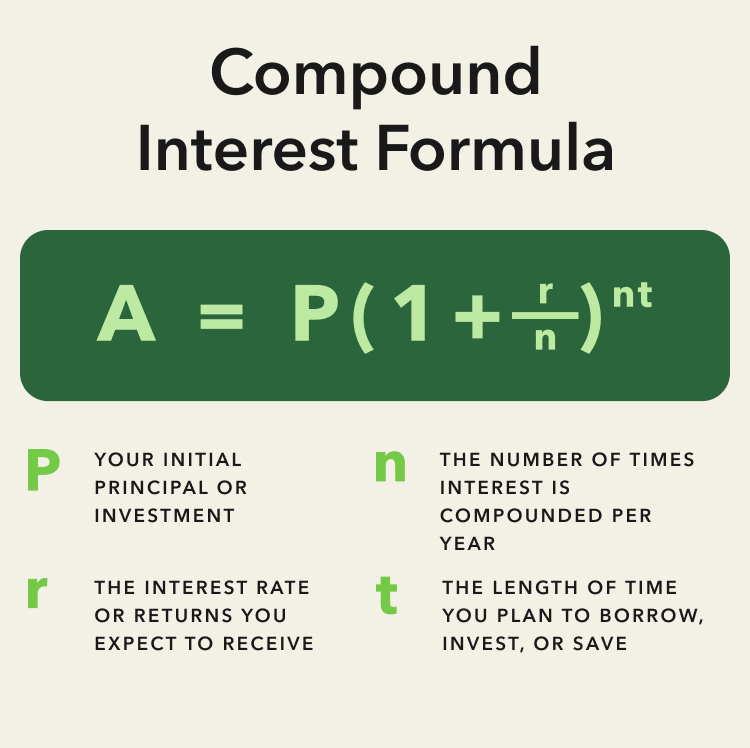

Finally, the type of interest calculation method employed by lenders can also impact the total interest paid. Some lenders use a simple interest calculation method, while others employ the compound interest method. With compound interest, the interest is calculated not only on the principal amount but also on the accumulated interest over time. This can significantly increase the total interest paid, making it essential to understand the interest calculation method used by the lender before committing to a loan.

Understanding how loan terms affect interest calculations is crucial for making informed financial decisions. By delving into the world of loans through this comparative analysis, we have shed light on the importance of interest rates, repayment periods, and interest calculation methods. Remember, careful consideration of these factors can save you a substantial amount of money in the long run. So, the next time you embark on a loan journey, armed with this knowledge, you can confidently choose the most favorable terms and embark on a path towards financial success!